.jpg)

Weekly Newsletter

Freedom Calls: 18/5/26, Everyone likes a good staycation… and what didn't happen in China

by

The Team at Freedom Asset Management

May 18, 2026

15 Minutes

Freedom Calls: 18/5/26, “Everyone likes a good staycation… and what didn't happen in China”

From the team at Freedom Asset Management

"Manhattan by the sea" a.k.a. Dubai…. everyone loves a good staycation

No wildlife photos this week, just wild life… and lots of articles.

Pictured: Dubai's Palm beach front looking out to the Marina district, May 2026

In Abu Dhabi, day-to-day business is quickly returning to normal and the restaurants are looking busy. However, Dubai is a very different economy and the tourists are notably missing. With strong travel advisories still in place from the UK, US and other governments, (effectively meaning travel insurance is void), Dubai is a quiet city.

Hotels are struggling; it is a bit like Covid times. On Wednesday, my longstanding overnight bolt-hole in Dubai's financial district (DIFC), the Ritz Carlton, was selling rooms for $200/night - and for that $200 we were given a hotel room the size of a small African country. I heard different numbers in Dubai last week; it seems 15-30% occupancy levels during the week are not uncommon. But Dubai hoteliers are nothing if not resourceful - a hastily revived "staycation" market has appeared. This has pushed occupancy on the Palm towards 70% at the weekends, as savvy UAE residents take advantage of amazing hotel deals and (still) great weather. When you can book a 5-star hotel room on the Palm for $170… you feel almost duty bound to support your fellow UAE businesses… and enjoy yourself at the same time!

What didn't happen in China

The plan this week was to write about the Trump/Xi summit in China. The problem is that there is not really much to write about. The newspapers have already dropped the story from the front pages.

We are essentially left with two narratives: (1) Iran has said they want a peaceful resolution in the Strait of Hormuz, and may decide to stop arming the Iranians… and (2) Xi has asked Trump to re-consider supplying arms to Taiwan. There was some warm stuff, and lots of selfies with Elon, but if you were looking for big read outs, this was not the summit.

The UK becomes "Italy" - just without the weather, or the food

England 5 - Italy 3. Sadly it's not a football result, it is the number of UK prime ministers vs Italian prime ministers since 2018. And it is about to change again with Starmer all but finished in the top job. Democracy is hitting a real problem; the traditional parties in the UK seem incapable of holding together a party and a mission. I wonder how much of this can be traced back to the increasing dominance of social media vs traditional media. It wasn't that long ago that the traditional media controlled the political narrative in the UK; that seems to be over now.

For our UK-based investors, it is helpful to remember that we have virtually no investments in the UK. So when the UK government goes to the dogs…. as it does frequently, and sterling sinks, the value of your investments with us, (which are in US dollars), go up in sterling terms. So this week the sterling numbers look good.

Back in the Gulf the ceasefire is broadly holding, but so is the blockade of the Strait of Hormuz

There is peace, but it is an uneasy peace. Daily missile warnings in the UAE are largely a thing of the past, but the Gulf has fissured in terms of support and strategy; it feels like a stalemate is looming. The UAE has gone all-in with the USA and Israel - and has brought over the "Iron Dome" to the UAE. The UAE wants the US to be more assertive against Iran.

Saudi is more reluctant; back in September 2025, Saudi signed a mutual defence pact with Pakistan, which "NATO Article 5 style" requires Pakistan to come to Saudi's aid if attacked. The point being that Pakistan is a nuclear power. On a side-note, anyone genuinely expecting Pakistan to start firing (nuclear or other) missiles at Iran, should Saudi come under attack, must be smoking something illegal - that feels wildly unlikely and if I were Saudi I certainly would not be relying on it.

The Saudis are trying to push a "Non Aggression Pact" with Iran, along the lines of the 1975 Helsinki Accords during the Cold War. It seems unlikely that this will get off the ground - the UAE is still furious with Iran, and I don't think anyone expects Israel to respect such a pact.

Interestingly, global stock markets seem relatively unbothered by the blockade of the Strait of Hormuz. The people I speak to in the Gulf are expecting this to last a few more months - that is not good for Asian markets reliant on Gulf fuel products, or for inflation in the US and further afield. But right now the story in the US is all about the power and growth of AI, which on its own, according to our tech team, could be worth about 3% p.a. of GDP growth. So that could carry global GDP growth on it own, even if the traditional world struggles.

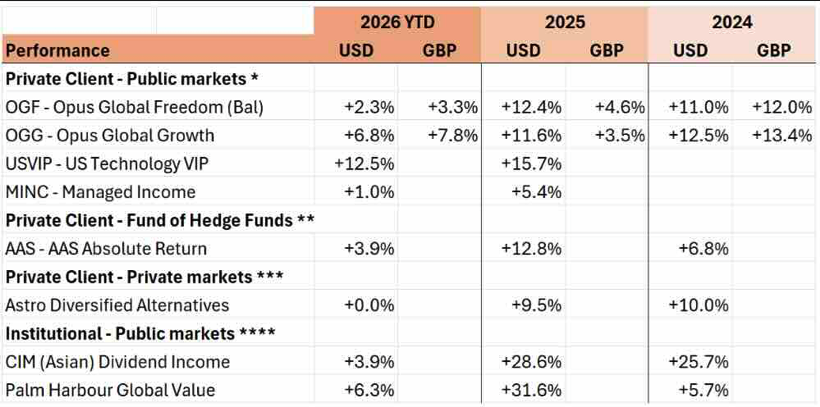

Performance

(For performance disclaimers, please see notes at the foot of this email).

It was definitely a week of two halves; a very punchy first half, and then a more disappointing second half. So we finished the week little changed from the numbers we published a week earlier with, as I like to say, plenty of embedded value left to realize in the funds. Therefore I believe there are plenty of reasons to feel positive about investing now.

During the week, in OGF we broadened out the defence exposure, which has not been working so well for us in the last 6 weeks. We sold a third of our global defence exposure to put that into a pure European defence exposure. There have been some big drawdowns at the European defence companies, like Rheinmetall, and this seems counter-intuitive against a backdrop of more and more defence expenditure being mandated, so this should give us greater upside capture to the theme.

The USVIP team took advantage of Palantir coming off about 25% from its highs this year to initiate a position in that name, alongside Shopify, which again was off about 40% from its recent highs. Both stocks are up since purchase.

I caught up with Justin Oliver this week in the UAE on OGG. He is happy to sit tight and his positioning has worked out well for the fund.

On MINC, Ramon has taken advantage of inflation fears, which pushed up yields at the longer end to buy some 7-10 year US treasuries, which should help build up the distribution yield.

Our articles this week:

Canaccord's Justin Oliver, Adviser to Opus Global Growth (OGG) writes about "Jerome Powell - the defender of Central Bank autonomy"

Freedom's Derek Akkiprik writes for us on the battle for Chinese LLMs in, "Beyond DeepSeek: The Rise of China’s LLM Ecosystem"

10,000 Days' Cody Willard, Adviser to US Technology VIP (USVIP) notes, "The AI Revolution is Still in the First Inning: Compute Bottlenecks, Neoscalers, and the Laser Age", and

and

Freedom's Charles Harris takes a look at Stanley Druckenmiller in our new series looking at the strategies of great investors.

Please scroll down to read the articles this week.

It is a busy week of travel for me this week, starting today in Abu Dhabi, tomorrow in Guernsey and by the end of the week in Hong Kong.

Remember next week is Eid, so a lot of firms in the Middle East will be closed for the public holidays.

Wherever you are, please let me wish you a safe and successful week ahead.

Adrian.

Co-Founder // Freedom Asset Management

Guernsey // Abu Dhabi // Hong Kong

M: +44 7781 40 1111 // M: +971 585 050 111 // M: +852 5205 5855

—————————————————

“Jerome Powell - the defender of Central Bank autonomy”, 18/5/26

By Canaccord’s Justin Oliver, Investment Adviser the Opus Global Growth Fund

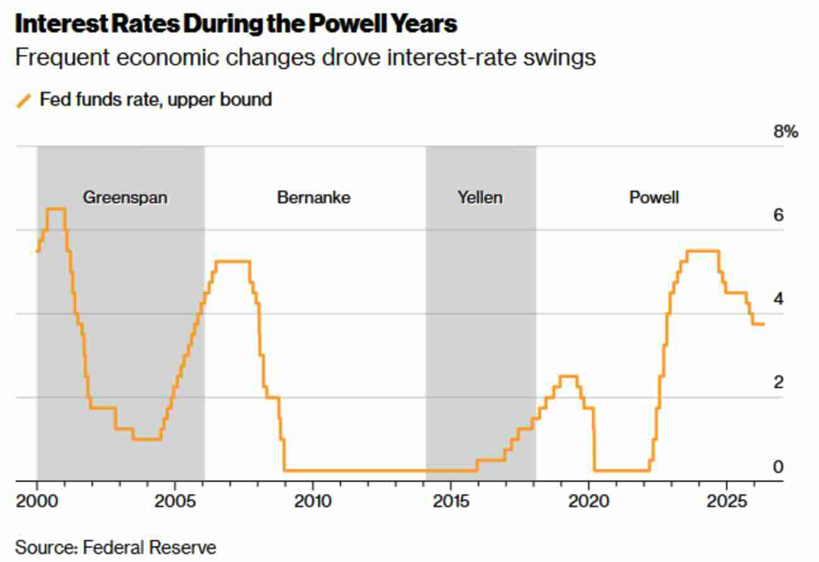

Jerome Powell’s tenure as Chair of the Federal Reserve is likely to be remembered for far more than interest-rate decisions alone. While his period in office encompassed one of the sharpest economic shocks in modern history, the defining feature of his legacy may ultimately be his defence of central bank independence in the face of escalating political pressure.

Powell inherited the role at a highly sensitive moment. Having previously worked in both finance and public service, including involvement in efforts to navigate the 2011 US debt-ceiling crisis, he was appointed to the Federal Reserve Board by President Barack Obama before later being elevated to Chair by Donald Trump. However, relations between the two deteriorated quickly. Trump publicly criticised Powell and the Fed with a frequency and intensity rarely seen in modern US political history, challenging a long-standing convention that monetary policy should remain insulated from day-to-day political influence.

The most severe test of Powell’s leadership initially came during the Covid-19 pandemic. Faced with a sudden economic shutdown and extreme market stress, the Federal Reserve moved aggressively to stabilise financial markets and support economic activity. Yet Powell repeatedly stressed that monetary policy alone would not be sufficient. In April 2020, he openly called on lawmakers to use “the great fiscal power of the United States” to support households and businesses. Congress ultimately responded with roughly $5 trillion of fiscal stimulus measures introduced under both Trump and Joe Biden.

By several measures, the response was remarkably effective. Although the pandemic recession was exceptionally deep, it proved historically short-lived, lasting only two months. By the end of 2021, unemployment had fallen back below 4%, highlighting the resilience of the US economy and the scale of the recovery effort. However, the rebound also brought an unintended consequence: the highest inflation experienced in decades. As economies reopened and demand surged, supply chains struggled to keep pace. Critics argued that both fiscal and monetary policy had remained too loose for too long, allowing inflationary pressures to become embedded. Powell himself faced scrutiny for initially characterising inflation as “transitory,” before the Federal Reserve was ultimately forced into one of the most aggressive rate-hiking cycles in recent history.

Despite these criticisms, Powell’s supporters contend that his leadership helped engineer an outcome many economists had previously viewed as improbable: a sharp decline in inflation without a deep and prolonged recession. The US economy slowed, but employment remained comparatively resilient, and the feared collapse in economic activity never fully materialised. Markets also adapted surprisingly well to higher interest rates, aided by strong corporate balance sheets and continued consumer spending. Yet as inflation concerns gradually eased, Powell entered another politically charged phase of his chairmanship. Renewed pressure from Trump and his allies intensified debates around the autonomy of the Federal Reserve, particularly as questions emerged over future rate cuts and the role of monetary policy in supporting growth. Powell repeatedly insisted that policy decisions would remain guided by economic data rather than political demands.

That stance increasingly became central to perceptions of his leadership. Bloomberg noted that Powell’s reputation as a defender of central bank independence was cemented when he publicly challenged investigations and criticism directed toward the institution during the Trump administration. In many respects, this battle over institutional credibility may prove as historically important as the Fed’s pandemic-era policy actions.

The broader significance extends well beyond Washington. Financial markets rely heavily on confidence that central banks can make difficult decisions without political interference. If investors begin to doubt that inflation will be controlled independently, borrowing costs can rise, currencies can weaken, and longer-term economic stability may be undermined. Powell’s determination to protect that independence therefore carried implications not just for the United States, but for the functioning of the global financial system.

As Powell steps aside as Chair while remaining on the Federal Open Market Committee as a regular member, debate over his economic record will undoubtedly continue. Some will focus on the inflation surge that followed the pandemic response, while others will highlight the speed of the recovery and the resilience of the labour market. Yet historians may ultimately judge that his greatest contribution was institutional rather than purely economic: preserving the Federal Reserve’s independence during a period of unusually intense political pressure. As Fed historian Peter Conti-Brown observed, Powell’s place in history may already be secure because of both the Covid crisis and the subsequent defence of central bank autonomy.

Justin Oliver

———————————————

"Beyond DeepSeek: The Rise of China’s LLM Ecosystem", 18/5/26

By Derek Akkiprik, Abu Dhabi analyst team

For much of the past decade, the assumption across global markets was that the United States would dominate the artificial intelligence race almost uncontested. Silicon Valley possessed the capital, semiconductor access, the research ecosystem, and the world’s leading technology firms. China, while seen as technologically capable, was often viewed as playing catch-up.

That perception has changed rapidly.

Over the last two years, Chinese large language models (LLMs) have evolved from domestic ChatGPT alternatives into increasingly credible global competitors. What began as a reactive push following OpenAI’s breakthrough has developed into something far more significant: a parallel AI ecosystem with its own strategy, strengths, and ambitions.

Following the release of ChatGPT in late 2022, Chinese technology firms moved aggressively to accelerate their own AI programs. Baidu launched Ernie Bot, Alibaba expanded its Qwen model family, while Tencent, ByteDance, and a growing number of startups entered the space. Early iterations often lagged their Western peers in reasoning ability and sophistication, but the pace of development was striking.

What makes China’s AI ecosystem particularly interesting is that it has not simply attempted to copy Silicon Valley. In many ways, it is evolving along a different path.

Western frontier labs such as OpenAI and Anthropic have largely pursued closed ecosystems built around proprietary models, premium subscriptions, and tightly controlled APIs. Chinese firms, by contrast, have increasingly leaned toward open-weight and open-source strategies, allowing developers broader access to models and accelerating adoption across domestic and international markets.

This difference became especially visible during what many investors now refer to as the “DeepSeek moment.”

When Chinese startup DeepSeek released its R1 reasoning model in early 2025, markets reacted immediately. The model reportedly achieved reasoning performance comparable to some leading Western systems while being developed at a fraction of the expected cost. The announcement triggered a sharp selloff across parts of the US technology sector as investors began reassessing one of the core assumptions underpinning the AI trade: that frontier AI leadership would require virtually unlimited capital expenditure and compute spending.

DeepSeek’s significance was not simply about benchmark performance. It highlighted something potentially more important, efficiency.

The graph above visualizes a subset of high-performing models from the Artificial Analysis Intelligence Index. These scores are calculated by testing the models across 10 different evaluations that measure practical skills like coding, scientific reasoning, and their ability to handle complex, real-world tasks.

US semiconductor export restrictions were originally designed to slow China’s AI development by limiting access to advanced chips. Instead, those constraints appear to have forced Chinese developers to optimize aggressively. Rather than relying purely on scale and computational brute force, many Chinese firms focused on reducing training costs, improving efficiency, and maximizing performance under tighter hardware limitations.

In many ways, necessity accelerated innovation.

State support has also been critical to China’s AI rise. Beijing increasingly views artificial intelligence as a strategic national priority alongside semiconductors, telecommunications, and energy infrastructure. Government support has flowed into AI infrastructure, domestic chip development, cloud computing, and research ecosystems, while state-linked institutions have actively promoted the adoption of domestic AI systems.

Unlike Silicon Valley’s largely venture-capital-driven model, China’s AI sector operates much closer to an industrial policy framework where government strategy and corporate development are deeply interconnected.

That said, important differences between Chinese and Western LLMs remain. American firms still retain meaningful advantages in cutting-edge semiconductor access, global cloud infrastructure, and premium enterprise adoption. At the same time, Chinese models continue to face scrutiny regarding censorship, political alignment, and regulatory oversight, particularly on politically sensitive topics.

Still, dismissing Chinese AI as derivative increasingly feels outdated.

Companies such as Alibaba, Tencent, Baidu, DeepSeek, Moonshot AI, and MiniMax are now producing systems that are globally competitive in several areas. More importantly, China’s AI ecosystem is beginning to establish its own identity rather than merely replicating Western models.

The broader implication is that the global AI race is no longer a single-track American story. Instead, two competing ecosystems are emerging simultaneously: Silicon Valley’s capital-intensive, closed-model approach and China’s increasingly efficient, open-weight alternative.

The question now may not simply be who builds the most powerful AI model. It may ultimately be which ecosystem proves more scalable, adaptable, and globally influential over the next decade.

This article sources data from UOB Kay Hian's recent report, "China AI LLM Winners". If you would like a copy of the full report, please let us know and we will be happy to put you in touch with the team at UOB Kay Hian.

Derek Akkiprik

—————————————

“The AI Revolution is Still in the First Inning: Compute Bottlenecks, Neoscalers, and the Laser Age”, 18/5/26

By the team at 10,000 Days, Investment Advisers to the US Technology VIP Fund

We are currently living through a technological inflection point that changes everything, yet we are barely scratching the surface of what is to come. Over the last three years since the initial “ChatGPT Moment”, we have watched AI transition from a mere novelty to something quietly but fundamentally integrated into our daily routines.

People are organically leaning on platforms like Gemini to figure out how to unshrink a sweater or identify strange buildup in a new fish tank and just about anything else they used to “Google”. But despite this broad and rapid consumer-level integration, corporate adoption is remarkably far behind. Just look at video games like Madden where we are still dealing with canned, stock voiceovers instead of real-time, dynamically generated commentary or how many tech companies like Amazon and others are literally grading their employees on AI-usage rather than AI-productivity. The promise of AI’s impact on the enterprise hasn’t even started.

The reality? We are maybe halfway through the first inning of the AI revolution going mainstream.

In the tech world, software and cloud-based businesses are almost always constrained by user demand. AI has flipped that paradigm entirely. Today, AI development is almost 100% gated by the supply side—specifically, how much compute power a company can get its hands on.

Companies like Anthropic and OpenAI are sitting on what equates to trillions of dollars in backlog simply because they cannot secure enough processing power. This desperate need for compute is why we keep seeing what seems like the same headlines over and over… companies like Anthropic, flush with capital, secure billions of dollars of access to compute from data centers like "Colossus," the giant AI factory and data center built by Elon Musk’s xAI for Grok.

Revolutions of this scale inevitably create tens of trillions of dollars in economic activity. The math scales dizzyingly fast: if a company like Anthropic is doing tens of billions now on something like 2000%+ topline growth, a 10x jump from here takes them to $300 billion, and another 10x takes them to $3 trillion in revenue. The market is actively trying to price in this massive economic and societal shift. Just weeks after market panic over geopolitical tensions, AI infrastructure stocks surged 30% to 50%, reflecting the sheer inevitability of this growth.

Building out the infrastructure to support this compute demand requires staggering capital. We are looking at nearly $1 trillion in capital expenditure on data centers in the US alone this year—up from $100 billion. That spend represents roughly 2.5% of the US nominal GDP ($38 trillion).

Naturally, there is political and social backlash. People worry about the massive strain on the energy grid and rising electricity prices and so on. But there is a flip side to this infrastructure boom:

Grid Stabilization: Like crypto-mining operations, modern data centers are increasingly built with their own independent energy generation. During peak load times (like summer heat waves), excess capacity from these centers will likely be routed back to stabilize the grid and keep prices low.

The "Percolative" Economic Effect: Spending $1 trillion on physical infrastructure creates a massive, localized economic boom. It requires pipe fitters, plumbers, electricians, and Caterpillar tractors and so on. It drives business to local restaurants serving those two-year temporary workers, and pays the waitresses who then buy local daycare. The economic steam rises and percolates through the entire economy, creating a massive, self-reinforcing flywheel.

This isn't a one-off spend. The flywheel of "AI creating AI that uses AI to create more AI" likely means that this level of investment will be sustained for a 10- to 20-year cycle, driven by what is currently somewhere around an incredible 30% to 40% Return on Investment (ROI).

So, what does this massive compute power actually do for productivity?

Imagine you need to put a hole in a wall. Technology often focuses on making a powerful drill and/or a sharper drill bit. Software, chips, applications, services -- everything in technology is about making the hole in the wall. AI is different. It's never been about the drill or the drill bit. AI is a laser that instantly blasts a hole through the wall nearly for free.

This level of efficiency will fundamentally change the workforce. While low-level, low-value coding jobs may not return, the ease of use of AI will create boundless new opportunities. Because AI understands natural language, anyone with internal drive can build hyper-specific, one-off applications for their personal lives.

Complex Travel Planning: Imagine asking an AI to instantly build a custom app that tracks a grueling 10-day itinerary spanning 16 airports, 8 flights, a train, two boats, and two countries (an example of a real trip I just recently completed, by the way), complete with live map visualizations.

Custom Healthcare Tracking: Consider a parent with a medically fragile child who uses AI to build a highly customized, secure daily medical log to track medications and biological functions (again, a real life example of my own)—something that was too complex to code just a year and a half ago when I last tried to build it, but is entirely possible today as I try it again and am blown away by the improvements in this AI capability over just the last year and a half.

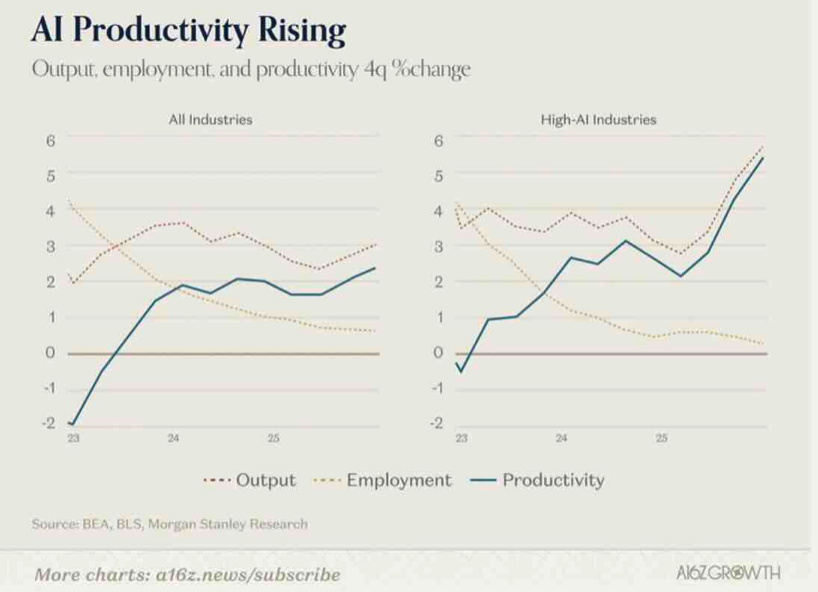

And again, we’re just now getting to the inflection point of enterprises using AI across industry making a huge productivity boom inevitable in coming years:

These charts are hockey sticking here and they’re just getting started.

While everyone is focused on the AI software revolution, the robotics revolution is quietly inflecting right alongside it. We are having the "ChatGPT moment" of robotics right now.

Robots are already here, working in industries that have never used them before. We have laser-equipped robots shooting weeds on farms in rural New Mexico, and drones tying rebar and hanging sheetrock in high-rise construction sites in Abu Dhabi.

On the consumer front, companies like Tesla are pushing the boundaries. The integration of AI into Tesla's Full Self-Driving (FSD) technology has reached a point of competence where it is fundamentally changing public perception. One anecdotal example shared on the call involved a father, initially skeptical, having a Tesla autonomously drive him home from a hospital appointment without him ever touching the wheel. By Mother's Day, he had bought his own Model Y, remarking to me out of the blue as he grilled burgers, "Boy, I love that Tesla" and proceeded to talk about it until the burgers were done.

When it comes to humanoid robots like Tesla's Optimus, the strategy is clear. Unlike competitors running "performative" gimmicks like robot half-marathons in China, Tesla aims to release a holistic, turnkey product. Elon Musk knows from the 15-year FSD journey that you must deliver a product with everyday utility from day one. Don't expect widespread Optimus rollouts immediately—likely not until version 4 next year—but when they arrive, they are poised to dominate the category. And don’t expect a flow of constant videos showing off the latest Optimus advancements because Elon doesn’t want competitors trying to emulate Tesla’s always unique and always first-principles approach.

To wrap up then: We have moved from the hammer, to the drill, and now to the laser. The only question left is: what comes after the laser, when we no longer even need to put a hole in the wall? Perhaps that's when we realize we're just living in a simulation. Haha (not haha? LOL).

At any rate, I continue to believe that the best -- and safest -- long-term ways to invest in these incredibly impact Tech Revolutions are by sticking with the companies that are building the most dominant platforms that all these AI and Robotics Revolutions will be built upon, which is exactly what so much of our portfolio is focused on: Google, Apple, Nvidia, ARM Holdings, Synopsis, to name a few. I’ve spent my entire professional career analyzing and investing in these Revolutions and while we remain mindful of the geopolitical tensions and outright wars that are clearly still issues that can escalate into crises, these current burgeoning Revolutions are bigger and more inevitable than any other of our lifetimes, which means the long-term outlook is as bright as I’ve ever seen it.

Cody Willard

——————————

"Legendary Investors - Part 1: Stanley Druckenmiller", 18/5/26

By Charles Harris - Investment Team Abu Dhabi

Few investors have a track record quite as immaculate as that of Stanley Druckenmiller. Over a 30-year period, between 1981 to 2010, he achieved a staggering +30% compound annualized growth rate (CAGR) without a single down year. His career provides a masterclass in macroeconomic investing; his success is not based on any secret formula, but rather a disciplined patient and approach.

After dropping out of an economics PhD programme at the University of Michigan, Druckenmiller joined Pittsburgh National Bank in 1977. Two years later, came his first breakthrough as he watched the Iranian Revolution unfold and anticipated a spike in oil prices; he bet big on oil (70%) and defence (30%) stocks (100% long), the bet doubled whilst the S&P 500 remained flat.

In 1981, at 28 years old, he left and set up Duquesne Capital Management with $1m in seed capital. Following years of consistent performance he started managing external funds, in 1985 he became a consultant for Dreyfus and eventually moved to New York.

Black Wednesday

In 1988, George Soros hired Druckenmiller as the lead portfolio manager to the Quantum fund. It’s during his period at the Quantum fund that Druckenmiller made his most famous bet against the British Pound – on ‘Black Wednesday’. Whilst Soros is generally credited, Druckenmiller was the man who identified the opportunity and orchestrated the trade. Druckenmiller identified a macro misalignment where Britain needed to lower interest rates to stimulate its economy and help mortgage holders but was forced to keep interest rate artificially high to maintain its peg with Germany which was unsustainable and made the devaluation of the Pound inevitable.

Druckenmiller approached Soros suggesting a bet of $1.5bn of the $7bn fund against the pound given the limited downside potential (Sterling was already at its lowest level) and high upside potential (if the peg were to break, sterling would likely collapse 20%+). Soros dismissed the size of the bet and told him to, “go for the jugular” and increased the short position to c. $10bn - leveraging the fund. When sterling was finally devalued the trade ended up netting a $1bn profit.

After Quantum

But it did not always go to plan. Druckenmiller left Quantum fund in April 2000 following a painful $3bn loss, succumbing to FOMO (fear of missing out). In January 2000 he sold all his tech positions believing valuations were egregious, by March he bought back $6bn worth of tech stocks just as the market peaked – losing $3bn in the following six weeks.

After admitting he had become an “emotional basket case” and taking a brief sabbatical, he returned to manage Duquesne in September. Astoundingly, he managed to finish the year up - by building a long position in 30Y US Treasuries just before the economy weakened, and bond yields plummeted providing a massive performance boost. He continued to manage external capital at Duquesne until 2010 when he closed it to external investors, citing the “high emotional toll” of maintaining a pristine track record and now solely manages his personal wealth through his family office.

I picked up several lessons when looking at his approach.

The Key Lessons:

Capital Preservation above all else - "The way to build superior long-term returns is through preservation of capital and home runs." Above all else, protecting capital is vital for long-term performance and it has little to do with being safe or conservative but rather keeping capital available for when real opportunities arise. Loss of capital is seen as a loss of future compounding potential. He only takes bets with asymmetric profiles, rarely entering a trade unless the upside is significantly higher than the downside. He is perfectly comfortable sitting on his hands when there is no clear trend or high conviction opportunity, most investors lose money by toying with mediocre investments which eat away at capital needed for greater opportunities.

High Conviction/Aggressive Concentration – "I like putting all my eggs in one basket and then watching the basket very carefully." He often states that the key thing he learnt from his mentor George Soros was not some revolutionary macroeconomic viewpoint, but rather position sizing – citing that “It is probably 70% to 80% of the equation. It is not just about being right or wrong, it is about how much you make when you’re right, and how much you lose when you’re wrong.”

Invest in the future – "Never, ever invest in the present." Rooted in the belief that current stock prices reflect what the world knows (e.g. headline news). To make money you should visualise 18-24 months out; the timeframe is suitably far enough that the consensus is often wrong, and fundamental catalysts can already be in motion. The trick is to not just look for good companies, but what will make people think differently about a company in the future. He is notably indifferent to quarterly earnings unless they change the long-term thesis.

Top-down macro picture - “Earnings don't move the overall market; it's the Federal Reserve Board... focus on the central banks, and focus on the movement of liquidity”. The expansion and contraction of money supply within the financial system creates the necessary conditions for price movement, he therefore focuses intensely on central bank policy. He also monitors yield curve and credit spreads as indicators of when liquidity is expanding or contracting. He uses liquidity and technical analysis to decide when to buy, and fundamental analysis to decide what to buy.

"Invest then investigate" – this is a way of handling intuition and timing, before doing a deep dive he would initiate a small position to have skin in the game, this allows him to listen to the news and watch its stock price action with more concentration.

Extreme flexibility – One of the reasons he left Quantum was just the sheer volume of assets he was managing ($14bn in early 2000). He recalled feeling like the “Titanic”. At Duquesne he was able to move in and out of the market far more efficiently.

Know when to call quits – reducing positions and clearing your head, being emotionally detached from any position and being able to close the position no matter what the entry price was.

Contrarianism with conviction – “contrarianism for its own sake is overrated” – he only takes a contrarian stance when research provides extreme conviction. As he says, the market tends to be right 80% of the time.

We can learn a lot from great investors. Although there can be a tendency to think that conditions are different now, and there is access to a great deal more financial information than when Druckenmiller was making his big bets against sterling, the reality is often that more information is just noise, and we do well to stick to simple rules to deal with the information.

We will be covering more legendary investors over the coming weeks.

Charles Harris

—————————————

Disclaimers

Performance table

Capital at risk. Returns in US dollars unless otherwise stated.

Sources:

* Estimates Freedom Asset Management as at 16/5/26. Please note depending upon how the funds are invested a small number of underlying funds can price 1-2 days after we take our estimates above so final published NAVs may vary. Estimated GBP returns are from a $1.25 FX rate on 31/12/24 and $1.34 as at 31/12/25. Please note launch dates of USVIP 12/2/25 and MINC 20/5/25.

** Performance estimated from JP Morgan supplied estimates, using Class B shares. Fund prices monthly, with monthly subscriptions and quarterly (qtr/90) redemptions.

*** Note fund prices quarterly and includes 5% discount to NAV expressed as 5% performance above for 2024, note also that the 2025 estimate takes the MCAS December 2025 estimate and deducts the estimated charges of the Astro feeder fund.

**** Morningstar as at 16/5/26, I shares for CIM Dividend Fund, F shares for PHC Global Value Fund.

General

If you would like to be removed from this Monday morning mail, please reply ‘unsubscribe’.

Capital at risk. For further details about any of Freedom’s investment strategies or a copy of any fund prospectus, please contact investor@freedomasset.com. Please note: The value and the income produced by strategies may fluctuate, so that an investor may get back less than initially invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Levels and bases of taxation may change. Investors should consult their own tax advisor regarding their individual tax treatment with respect to the strategies referred to herein. This document does not represent a research report. The opinions expressed are those of the authors only, and may not be representative of, or shared by, Freedom Asset Management Limited or its affiliates. This email should not be considered to be an offering memorandum and is not an offer to sell nor a solicitation of an offer to purchase interests in any fund. Offers and sales will be made only pursuant for the current prospectus, constituent documentation and in accordance with applicable securities laws. A decision to invest in any of the funds should only be based upon review of such documents and these materials are qualified in their entirety by reference thereto.

Please note Freedom’s investment strategies are only available to Professional Investors, as determined by the relevant jurisdiction.

This message is intended solely for the addressee and may contain confidential or privileged information. If you have received this message in error, please permanently delete it and do not use, copy or disclose it. Freedom Asset Management Limited is licensed to carry on controlled investment business under the Guernsey Financial Services Commission (GFSC); Reference Number 2262946. The registered office of Freedom Asset Management Limited is: 2nd Floor, New Century House, 2 Jubilee Terrace, St Peter Port, Guernsey, GY1 1AH, Channel Islands. Freedom Asset Management (Middle East) Limited is authorised and regulated by Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority, No: 250016. The registered office address of Freedom Asset Management (Middle East) Limited is Office 2406, Tamouh Tower, Al Reem Island, Abu Dhabi Global Markets, Abu Dhabi, United Arab Emirates. Freedom Asset Management (Asia) Limited, holds a Type 9 Asset Management license from the Securities and Futures Commission in Hong Kong, Ref: BUR351. The registered office of Freedom Asset Management (Asia) Limited is Unit 2117, Level 21, New World Tower 1, 16-18 Queen's Road Central, Hong Kong.

© 2026 Freedom Asset Management Limited.